Peppol International (PINT) model for Billing

OpenPeppol AISBL, Post-Award Coordinating Community v1.1.3

Link to main site of documentation

Introduction

This Peppol Business Interoperability Specification (BIS) is a national customization of global PINT for Oman. This specification is designed to facilitate interoperability and streamline the eInvoice process, incorporating local adaptions to meet Oman’s legal mandates and business needs.

The purpose of this document is to describe the use of the invoice and credit note messages in Peppol, and to facilitate an efficient implementation and increased use of electronic collaboration regarding the billing process based on these formats.

Document Structure

This document is structured as follows:

-

Chapter 1 gives general information on the business processes, requirements and functionalities.

-

Chapter 2 provides information on business related requirements supported by the invoice.

-

Chapter 3 provides information on legal and tax related requirements supported by the invoice.

-

Chapter 4 provides information about rules and calculations that applies to the invoice content.

-

Chapter 5.1 describes the BIS identifiers.

-

Chapter 5.2 describes the semantical data types.

-

Chapter 5.3 gives external links to the relevant UBL schemas.

Scope

This document is concerned with clarifying requirements for ensuring interoperability and provides guidelines for the support and implementation of these requirements. This document provides a detailed implementation guideline for the invoice and credit note transactions.

Audience

The audience for this document is organisations wishing to be Peppol enabled for exchanging electronic invoices, and/or their ICT-suppliers. These organisations may be:

-

Service providers

-

Contracting Authorities (CA)

-

Economic Operators (EO)

-

Software Developers

More specifically, roles addressed are the following:

-

ICT Architects

-

ICT Developers

-

Business Experts

For further information on Peppol/OpenPEPPOL see http://peppol.org

Benefits

The invoice and credit note provides simple support for invoicing where there is a need for credit note in addition to an invoice. Other potential benefits are, among others:

-

Can be mandated as a basis for national or regional eInvoicing initiatives.

-

Procurement agencies can use them as basis for moving all invoices into electronic form. The flexibility of the specifications allows the buyers to automate processing of invoices gradually, based on different sets of identifiers or references, based on a cost/benefit approach.

-

SME can offer their trading partners the option of exchanging standardised documents in a uniform way and thereby move all invoices/credit notes into electronic form.

-

Large companies can implement these transactions as standardised documents for general operations and implement custom designed bi-lateral connections for large trading partners.

-

Supports customers with need for more complex interactions.

-

Can be used as basis for restructuring of in-house processes of invoices.

-

Significant saving can be realised by the procuring agency by automating and streamlining in-house processing. The accounting can be automated significantly, approval processes simplified and streamlined, payment scheduled timely and auditing automated.

1. Business processes

1.1. Parties and roles

The diagram below shows the roles involved in the self-billed invoice and self-billed credit note transactions. In a self-billing arrangement, the Customer acts as the invoice issuer (sender), while the Supplier acts as the invoice receiver.

1.1.1. Parties

- Customer

-

The customer is the legal person or organisation who is in demand of a product or service. In a self-billing context, the Customer acts as the invoice issuer. Examples of customer roles: buyer, consignee, debtor, contracting authority.

- Supplier

-

The supplier is the legal person or organisation who provides a product or service. In a self-billing context, the Supplier remains the taxable party and acts as the invoice receiver.

1.1.2. Roles

- Creditor

-

One to whom a debt is owed. The party that claims the payment and is responsible for resolving billing issues and arranging settlement. In a self-billing context, this is the Supplier.

- Debtor

-

One who owes debt. The party responsible for making settlement relating to a purchase. In a self-billing context, this is the Customer, who also issues the invoice.

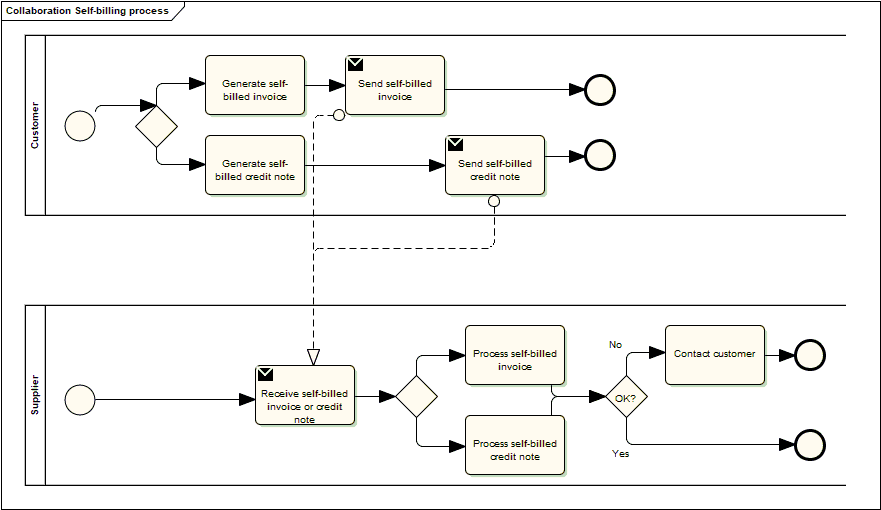

1.2. Self-Billing process

The self-billing process includes the creation, issuance, and transmission of the invoice and credit note by the Customer (acting as invoice issuer) to the Supplier (acting as invoice receiver), and the reception and processing of the same at the Supplier’s site.

In a self-billing scenario, the Customer assumes the role of invoice issuer, while the Supplier remains the Creditor from a commercial perspective.

The invoicing process is shown in this workflow:

-

A customer (acting as invoice issuer) creates and sends a self-billed invoice to a supplier. The invoice refers to one order and a specification of delivered goods and services.

An invoice may also refer to a contract or a frame agreement. The invoice may specify articles (goods and services) with article number or article description.

-

The supplier receives the self-billed invoice and processes it in their accounting or invoicing system.

The diagram below shows the basic self-billing process with the use of this Peppol BIS profile. This process assumes that both the self-billed invoice and the self-billed credit note are exchanged electronically.

This profile covers the following invoice processes:

| P1 |

Invoicing of deliveries of goods and services against purchase orders, based on a contract |

| P2 |

Invoicing deliveries of goods and services based on a contract |

| P3 |

Invoicing the delivery of an incidental purchase order |

| P4 |

Pre-payment |

| P5 |

Spot payment |

| P6 |

Payment in advance of delivery |

| P7 |

Invoices with references to a despatch advice |

| P8 |

Invoices with references to a despatch advice and a receiving advice |

| P9 |

Credit notes or invoices with negative amounts, issued for a variety of reasons including the return of empty packaging |

1.3. Invoice functionality

An invoice may support functions related to a number of related (internal) business processes. This Peppol BIS shall support the following functions:

-

Accounting

-

Invoice verification against the contract, the purchase order and the goods and service delivered

-

Tax reporting

-

Auditing

-

Payment

In the following chapters an assessment is made of what information is needed for each of the functions listed above and whether it is in scope or out of scope for this Peppol BIS.

Explicit support for the following functions (but not limited to) is out of scope:

-

Inventory management

-

Delivery processes

-

Customs clearance

-

Marketing

-

Reporting

1.3.1. Accounting

Recording a business transaction into the financial accounts of an organization is one of the main objectives of the invoice. According to financial accounting best practice and TAX rules every taxable person shall keep accounts in sufficient detail for tax to be applied and its application checked by the tax authorities. For that reason, an invoice shall provide the information at document and line level that enables booking on both the debit and the credit side.

1.3.2. Invoice verification

This process forms part of the Supplier’s internal business controls in a self-billing context.

The Supplier (as invoice receiver) shall verify that the self-billed invoice correctly reflects the underlying commercial transaction.

Support for invoice verification is a key function of an invoice. The invoice should provide sufficient information to look up relevant existing documentation, electronic or paper, for example, and as applicable:

-

the relevant purchase order

-

the contract

-

the call for tenders, that was the basis for the contract

-

the Customer’s reference

-

the confirmed receipt of the goods or services

-

delivery information

The invoice should also contain sufficient information that allows the received invoice to be transferred to a responsible authority, person or department, for verification and approval within the Supplier organisation.

1.3.3. Auditing

Companies audit themselves as means of internal control or they may be audited by external parties as part of a legal obligation. Accounting is a regular, ongoing process whereas an audit is a separate review process to ensure that the accounting has been carried out correctly. The auditing process places certain information requirements on an invoice. These requirements are mainly related to enable verification of authenticity and integrity of the accounting transaction.

Invoices, conformant to this PEPPOL BIS, support the auditing process by providing sufficient information for:

-

identification of the relevant Customer and Supplier

-

identification of the products and services traded, including description, value and quantity

-

information for connecting the invoice to its payment

-

information for connecting the invoice to relevant documents such as a contract and a purchase order

1.3.4. Tax Reporting

The invoice is used to carry tax-related information from the Supplier (as the taxable party) to the Customer, even though the invoice is issued by the Customer under a self-billing arrangement.

An invoice should contain sufficient information to enable the Customer and any auditor to determine whether the invoice is correct from a tax point of view.

The invoice shall allow the determination of the tax regime, the calculation and description of the tax, in accordance with the relevant legislation.

1.3.5. Payment

An invoice represents a claim for payment from the Supplier (Creditor), even when the invoice is issued by the Customer under a self-billing arrangement.

The issuance of an invoice may take place either before or after the payment is carried out. When an invoice is issued before payment it represents a request to the Customer to pay, in which case the invoice commonly contains information that enables the Customer, in the role of a debtor, to correctly initiate the transfer of the payment, unless that information is already agreed in prior contracts or by means of payment instructions separately lodged with the Customer.

If an invoice is issued after payment, such as when the order process included payment instructions or when paying with a credit card, online or telephonic purchases, the invoice may contain information about the payment made in order to facilitate invoice to payment reconciliation on the Customer side. An invoice may be partially paid before issuing such as when a pre-payment is made to confirm an order.

Invoices, conformant with this specification, should identify the means of payment for settlement of the invoice and clearly state what payment amount is requested. They should provide necessary details to support bank transfers. Payments by means of Credit Transfer, Direct debit, and Payment Card are in scope.

1.4. Credit notes and negative invoices

Reverting an invoice that has been issued and received can be done in two basic ways: either by issuing a credit note or a negative invoice. In a self-billing context, the corresponding document type codes for invoices and credit notes are '389' (self-billed invoice) and '261' (self-billed credit note), while the accounting principles described below remain unchanged.

-

When crediting by means of a credit note, the document type code is '381' (or its synonym), or '261' in the case of a self-billed credit note. The credit note quantities and extension/total amounts have the same sign (plus or minus) as the invoice that is being cancelled or credited. The document type code acts as an indicator that the given amounts are booked in reverse and cancel out the invoice amounts.

-

When crediting by means of a negative invoice, the document type code is '380' (or its synonym), or '389' in the case of a self-billed invoice. The negative invoice quantities and extension/total amounts have the opposite sign (minus versus plus) as the invoice being cancelled or credited. It is the mathematical sign that indicates that when the amounts are booked they cancel out the original amounts. The Price Amount must always be positive.

A credit note may include negative amounts when cancelling an invoice that may have negative line items or amounts.

1.5. Oman Business Processes

This section describes the business processes, document types, transaction models, and validation principles supported by the PINT Oman billing specification.

The rules defined in this section provide the business interpretation layer used for validation and interoperability.

1.5.1. Supported Document Types

The following business document types are supported in PINT Oman.

| Document Type | Code | Description |

|---|---|---|

Tax Invoice |

|

Standard tax invoice issued by the supplier |

Credit Note |

|

Credit note issued to adjust or reverse a previous invoice |

Self-Billing Invoice |

|

Invoice issued by the buyer on behalf of the supplier under a self-billing agreement |

Self-Billing Credit Note |

|

Credit note issued on behalf of seller. Self-billed credit notes can also be issued in cases other than self-billing arrangements, such as imports. |

1.6. PINT Oman Validation Rules (IBR-OM)

This section defines the validation principles and business constraints derived from the PINT Oman Schematron validation model.

1.6.1. Validation Scope

Validation applies to the following UBL document types.

| UBL Document | Scope |

|---|---|

|

Validation of invoices and self-billing invoices |

|

Validation of credit notes and self-billing credit notes |

Validation includes:

-

Transaction type interpretation

-

VAT validation

-

Currency consistency

-

Business scenario validation

-

Structural integrity checks

-

Context-specific business constraints

1.6.2. Transaction Type Model (BTOM-001)

General Principles

The transaction type (BTOM-001) is the primary driver for validation and business interpretation.

|

All validation rules MUST be interpreted in the context of the transaction type. |

The transaction type determines:

-

Mandatory business terms

-

Allowed combinations

-

VAT treatment

-

Scenario-specific validation rules

-

Conditional business requirements

Structure

The transaction type is represented as:

20-character bitmap of '1' and '0'Pattern:

[01]{20}A 1 marks an active transaction type at that position; every other position MUST be 0. The value MUST contain at least one 1.

Base Constraints

| Constraint | Requirement |

|---|---|

Position 1 |

Indicates Full Tax Invoice |

Position 2 |

Indicates Simplified Invoice |

Base invoice requirement |

Either Position 1 OR Position 2 MUST be |

Bit Mapping

| Position | Meaning |

|---|---|

1 |

Full Tax Invoice |

2 |

Simplified Invoice |

3 |

Self-Billed |

4 |

Third Party |

5 |

Summary Invoice |

6 |

Continuous Supply |

7 |

Export |

8 |

Deemed Supply |

9 |

Import Reverse Charge (RCM) |

10 |

Profit Margin |

11 |

Profit Margin Self-Invoice |

12 |

E-Commerce |

13 |

Import of Goods |

14 |

Special Zone |

15 |

Prepayment |

1.6.3. Conditional Mandatory Data

Certain business terms become mandatory depending on the transaction type.

| Condition | Required Data |

|---|---|

Export |

|

Summary Invoice |

|

Continuous Supply |

|

Third Party |

|

Import of Goods |

|

Prepayment |

|

Special Zone |

|

1.6.4. Core Header Rules

Identification Rules

The following identification rules apply.

| Validation Area | Requirement |

|---|---|

Transaction type |

MUST exist |

Transaction type format |

MUST be a 20-character bitmap of '1' and '0' ( |

UUID ( |

MUST be a valid UUID and MUST be version 5 (name-based, SHA-1) — see UUID Format (Version 5 / Version 4) |

UUID Format (Version 5 / Version 4)

Document UUIDs in PINT Oman MUST conform to RFC 4122. The required UUID version depends on the business term.

| Business Term | UUID Version | Rule |

|---|---|---|

Invoice UUID ( |

Version 5 only |

|

Seller UUID ( |

Version 4 or Version 5 |

|

A version 5 UUID is name-based: it is generated deterministically by hashing a namespace identifier together with a name using SHA-1. The same namespace and name therefore always produce the same UUID, which makes the Invoice UUID (BTOM-002) stable and reproducible for a given document. A version 4 UUID is randomly generated.

The Invoice UUID (BTOM-002) MUST be version 5:

^[0-9a-fA-F]{8}-[0-9a-fA-F]{4}-5[0-9a-fA-F]{3}-[89abAB][0-9a-fA-F]{3}-[0-9a-fA-F]{12}$The Seller UUID (BTOM-004) MAY be version 4 or version 5:

^[0-9a-fA-F]{8}-[0-9a-fA-F]{4}-[45][0-9a-fA-F]{3}-[89abAB][0-9a-fA-F]{3}-[0-9a-fA-F]{12}$In both patterns the third group’s leading digit is the UUID version (5, or [45]), and the [89abAB] group enforces the RFC 4122 variant. Only these two elements are format-checked; other UUID-bearing references are validated for presence only.

1.6.5. VAT Rules

VAT Categories

| Code | Description | Validation Rule |

|---|---|---|

|

Standard Rated |

5% VAT MUST apply |

|

Exempt |

VAT MUST NOT be present |

|

Outside Scope |

VAT MUST NOT be present |

|

Zero Rated |

VAT amount MUST be |

1.6.6. Party Requirements

Buyer Requirements

| Scenario | Requirement |

|---|---|

Full / Export / Summary / E-Commerce / Profit Margin Invoice |

Buyer ID OR Buyer VAT ID MUST be provided |

Self-Billed / Import / RCM / Profit Margin Self-Invoice |

Buyer VAT ID is mandatory |

1.6.7. Special Business Scenarios

Export Transactions

Export transactions:

-

MUST contain delivery country information

-

MUST contain supporting documents where required

Summary Invoice

Summary invoices:

-

MUST contain invoice period

-

MUST remain within the same calendar month

Prepayment

Prepayment scenarios:

-

MUST contain prepaid amount

-

MUST contain reference invoice information

1.6.8. Document References

The following document reference requirements apply to:

-

Tax Invoice (

380) -

Credit Note (

381) -

Debit Note (

383) -

Self-Billed Credit Note (

261)

Mandatory Reference Information

| Reference Element | Requirement |

|---|---|

Original invoice ID |

MUST be provided where reference to a previous document is required |

Issue date |

MUST be provided |

UUID |

MUST be provided |

Reason code |

MUST be provided where applicable |

Prepayment reference |

MUST be provided for prepayment-related transactions |

|

Where the original invoice or prepayment invoice was issued prior to the implementation of mandatory e-invoicing and therefore does not contain a valid UUID, the following dummy UUID SHALL be used when a previous UUID reference is mandatory:

This dummy UUID SHALL only be used for references to legacy documents issued outside the e-invoicing system prior to go-live. If the referenced document contains a valid UUID, the actual UUID MUST be used. |

1.6.9. Governance Principles

| Principle | Description |

|---|---|

Transaction-driven validation |

Transaction type governs business interpretation and validation |

Strict combination enforcement |

Invalid transaction combinations are rejected |

VAT consistency |

VAT breakdown MUST reconcile with source data |

Currency integrity |

Cross-currency validation rules MUST be enforced |

Scenario enforcement |

Context-specific business rules MUST be satisfied |

Structural consistency |

UBL structures MUST comply with the defined semantic model |

2. Business information

In the subchapters below you find description of selected parts of the transaction.

2.1. Parties

The following roles may be specified. The same actor may play more than one role depending on the handling routine.

Further details on the roles/actors can be found in Roles.

2.1.1. Seller (AccountingSupplierParty)

Seller is mandatory information and provided in element cac:AccountingSupplierParty

<>

<cac:Party>

<cbc:EndpointID schemeID="0248">1XXXXXXX1</cbc:EndpointID>

(1)

<cac:PartyIdentification>

<cbc:ID schemeID="0088">7300010000001</cbc:ID>

(2)

</cac:PartyIdentification>

<cac:PartyName>

<cbc:Name>SupplierTradingName Ltd.</cbc:Name> (3)

</cac:PartyName>

<cac:PostalAddress>

<cbc:StreetName>Street Name</cbc:StreetName>

<cbc:AdditionalStreetName>Additional Street name</cbc:AdditionalStreetName>

<cbc:CityName>Singapore</cbc:CityName>

<cbc:PostalZone>Postal Zone</cbc:PostalZone>

<cbc:CountrySubentity>West district</cbc:CountrySubentity>

<cac:AddressLine>

<cbc:Line>Third address line</cbc:Line>

</cac:AddressLine>

<cac:Country>

<cbc:IdentificationCode>OM</cbc:IdentificationCode> (4)

</cac:Country>

</cac:PostalAddress>

<cac:PartyTaxScheme>

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID>

(5)

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID> (6)

</cac:TaxScheme>

</cac:PartyTaxScheme>

<cac:PartyTaxScheme>

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID>

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:PartyTaxScheme>

<cac:PartyLegalEntity>

<cbc:RegistrationName>SupplierOfficialName Ltd</cbc:RegistrationName> (7)

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID> (8)

<cbc:CompanyLegalForm>Private Limited Company</cbc:CompanyLegalForm>

</cac:PartyLegalEntity>

<cac:Contact> (9)

<cbc:Name>Contact name</cbc:Name>

<cbc:Telephone>Contact number</cbc:Telephone>

<cbc:ElectronicMail>contact email ID</cbc:ElectronicMail>

</cac:Contact>

</cac:Party>

</cac:AccountingSupplierParty>| 1 | Seller electronic address (ibt-034), mandatory, the identification scheme identifier shall be chosen from the Electronic Address Scheme (EAS) list. |

| 2 | Seller identifier (ibt-029), if used, the identification scheme identifier shall be chosen from the entries of the list published by the ISO/IEC 6523 maintenance agency. |

| 3 | Sellers trading name (ibt-028). |

| 4 | Sellers country code (ibt-040). |

| 5 | Seller tax registration ID (ibt-031). |

| 6 | Tax scheme for the sellers tax registration. Use the appropriate code for the sellers jurisdiction, such as VAT or GST. |

| 7 | Seller legal registrated name (ibt-027). |

| 8 | Seller legal registration identifier (ibt-030), if used, the identification scheme identifier shall be chosen from the entries of the list published by the ISO/IEC 6523 maintenance agency. |

| 9 | Seller contact (ibg-06). |

2.1.2. Buyer (AccountingCustomerParty)

Buyer is mandatory information and provided in element cac:AccountingCustomerParty

<cac:AccountingCustomerParty>

<cac:Party>

<cbc:EndpointID schemeID="0248">1XXXXXXX1</cbc:EndpointID>

(1)

<cac:PartyIdentification>

<cbc:ID schemeID="0002">FR23342</cbc:ID>

(2)

</cac:PartyIdentification>

<cac:PartyName>

<cbc:Name>BuyerTradingName AS</cbc:Name> (3)

</cac:PartyName>

<cac:PostalAddress>

<cbc:StreetName>Street Name</cbc:StreetName>

<cbc:AdditionalStreetName>Additional Street name</cbc:AdditionalStreetName>

<cbc:CityName>CN</cbc:CityName>

<cbc:PostalZone>Postal Zone</cbc:PostalZone>

<cac:AddressLine>

<cbc:Line>Third line</cbc:Line>

</cac:AddressLine>

<cac:Country>

<cbc:IdentificationCode>OM</cbc:IdentificationCode> (4)

</cac:Country>

</cac:PostalAddress>

<cac:PartyTaxScheme>

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID>

(5)

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID> (6)

</cac:TaxScheme>

</cac:PartyTaxScheme>

<cac:PartyLegalEntity>

<cbc:RegistrationName>Buyer Official Name</cbc:RegistrationName> (7)

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID> (8)

</cac:PartyLegalEntity>

<cac:Contact> (9)

<cbc:Name>Contact name</cbc:Name>

<cbc:Telephone>Contact number</cbc:Telephone>

<cbc:ElectronicMail>contact email ID</cbc:ElectronicMail>

</cac:Contact>

</cac:Party>

</cac:AccountingCustomerParty>| 1 | Buyer electronic address (ibt-049), mandatory, the identification scheme identifier shall be chosen from the Electronic Address Scheme (EAS) list. |

| 2 | Buyer identifier (ibt-046), if used, the identification scheme identifier shall be chosen from the entries of the list published by the ISO/IEC 6523 maintenance agency. |

| 3 | Buyer trading name (ibt-045). |

| 4 | Buyer country code (ibt-055), mandatory. |

| 5 | Buyer tax registration ID (ibt-048). |

| 6 | Tax scheme for the buyer tax registration. Use the appropriate code for the buyers jurisdiction, such as VAT or GST. |

| 7 | Buyer legal registered name (ibt-044). |

| 8 | Buyer legal registration identifier (ibt-047), if used, the identification scheme identifier shall be chosen from the entries of the list published by the ISO/IEC 6523 maintenance agency. |

| 9 | Buyer contact (ibg-09). |

2.1.3. Payment receiver (PayeeParty)

Payment receiver is optional information. If this information is not supplied, the seller is the payment receiver. When payee information is sent this is indicating that a factoring situation is being documented.

To reflect the assignment of an Invoice to a factor there is a need to:

-

have a disclaimer (notification notice) on the Invoice that the Invoice has been assigned to a factor. The disclaimer should be given using the Invoice note (IBT-22) on document level.

-

identify the Factor as the Payee

-

to have the bank account changed to favour of a Factor.

<cac:PayeeParty>

<cac:PartyIdentification>

<cbc:ID schemeID="0248">987654325</cbc:ID>

(1)

</cac:PartyIdentification>

<cac:PartyName>

<cbc:Name>Payee party</cbc:Name>

</cac:PartyName>

<cac:PartyLegalEntity>

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID>

(2)

</cac:PartyLegalEntity>

</cac:PayeeParty>| 1 | schemeID attribute is recommended for all party identifiers |

| 2 | schemeID attribute is recommended for party legal entity identifiers |

2.1.4. Sellers Tax Representative (TaxRepresentativeParty)

Tax representative party for the seller is relevant for sellers delivering goods and services in a country without having a permanent establishment in that country. In such cases information on the tax representative shall be included in the invoice.

<cac:TaxRepresentativeParty>

<cac:PartyName>

<cbc:Name>TaxRepresentative Name</cbc:Name>

</cac:PartyName>

<cac:PostalAddress>

<cbc:StreetName>Regent street 32</cbc:StreetName>

<cbc:AdditionalStreetName>Additional Street name</cbc:AdditionalStreetName>

<cbc:CityName>CN</cbc:CityName>

<cbc:PostalZone>Postal Zone</cbc:PostalZone>

<cbc:CountrySubentity>Subentity</cbc:CountrySubentity>

<cac:AddressLine>

<cbc:Line>Back door</cbc:Line>

</cac:AddressLine>

<cac:Country>

<cbc:IdentificationCode>OM</cbc:IdentificationCode>

</cac:Country>

</cac:PostalAddress>

<cac:PartyTaxScheme>

<cbc:CompanyID>1XXXXXXX1</cbc:CompanyID>

(1)

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:PartyTaxScheme>

</cac:TaxRepresentativeParty>| 1 | Tax identifier of seller tax representative (ibt-063) |

2.2. Delivery Details (Date and Location)

Delivery details may be given at document level.

Place and date of delivery is recommended, and should be sent unless this does not affect the ability to ensure the correctness of the invoice.

The delivery element contains information on name, address and delivery location identifier (cac:Delivery/cac:DeliveryLocation/cbc:ID) which may be used if the place of delivery is defined through an identifier. For example GLN (Global Location Number)issued by GS1.

<cac:Delivery>

<cbc:ActualDeliveryDate>2017-11-01</cbc:ActualDeliveryDate>

<cac:DeliveryLocation>

<cbc:ID schemeID="0088">7300010000001</cbc:ID>

<cac:Address> (1)

<cbc:StreetName>Delivery street 2</cbc:StreetName>

<cbc:AdditionalStreetName>Additional Street name</cbc:AdditionalStreetName>

<cbc:CityName>CN</cbc:CityName>

<cbc:PostalZone>Postal Zone</cbc:PostalZone>

<cac:AddressLine>

<cbc:Line>Gate 15</cbc:Line>

</cac:AddressLine>

<cac:Country>

<cbc:IdentificationCode>OM</cbc:IdentificationCode> (2)

</cac:Country>

</cac:Address>

</cac:DeliveryLocation>

<cac:DeliveryParty> (3)

<cac:PartyName>

<cbc:Name>Delivery party Name</cbc:Name>

</cac:PartyName>

</cac:DeliveryParty>

</cac:Delivery>| 1 | Deliver to address (ibg-15), the address to which goods and services invoiced were or are delivered. |

| 2 | Deliver to country code (ibt-080), mandatory |

| 3 | Deliver to party name (ibt-070), the name of the party to which the goods and services are delivered. |

2.3. References and attachments

Support for invoice verification is a key function of an invoice. The invoice should provide sufficient information to look up relevant existing documentation, electronic or paper.

| Any reference element should contain valid information, if you do not have a reference, the element should not be present in the instance document. |

The invoice and credit note transactions supports the following references to existing documentation:

2.3.1. Purchase order and sales order reference

The purchase order reference is a conditional business term. If the customer has issued a purchase order should be referenced by providing its identifier in the resulting invoice, otherwise the Buyer reference should be used (see Buyer reference).

If the purchase order is referenced at the invoice header level, the order reference element on line level can be used to state the relevant line numbers in the order .

A sales order is issued by the seller, confirming the sale of specified products and may be provided in the invoice.

| In the invoice, both a purchase order and a sales order reference can be given, but be aware that an invoice instance cannot reference a sales order, without providing the corresponding purchase order reference. |

<cac:OrderReference>

<cbc:ID>o-998877</cbc:ID> (1)

<cbc:SalesOrderID>so-12343</cbc:SalesOrderID> (2)

</cac:OrderReference>| 1 | Purchase order reference |

| 2 | Sales order reference |

2.3.2. Buyer reference

The buyer reference, known as Your ref, is conditional. An invoice shall have either the buyer reference or the order reference (see Purchase order and sales order reference)

The element is used for the reference of who ordered the products/services. Example being the name of the person ordering, employee number or a code identifying this person or department/group. Your ref is often used for internal routing at recipient, and hence it is important to fill this element with the correct values according to the need of the recipient.

If neither buyer reference nor a reference to an order is supplied by the customer, the name of the person ordering or appointed for the customer can be supplied in buyer reference if known by the supplier.

| When reference is provided by the customer, the correct element shall contain the provided reference. |

<cbc:BuyerReference>0150abc</cbc:BuyerReference>2.3.3. Invoiced object identifier

The invoiced object identifier is the identifier for an object on which the invoice is based, given by the Seller. Examples may be a subscription number, telephone number, meter point, vehicle, person etc., as applicable.

If it is not clear to the receiver what scheme is used for the identifier, an optional scheme identifier attribute should be used, that shall be chosen from the Invoiced object identifier scheme code list.

The invoiced object reference is provided by using the element cac:AdditionalDocumentReference with the document type code = 130

<cac:AdditionalDocumentReference>

<cbc:ID schemeID="ABT">DR35141</cbc:ID> (1) (2)

<cbc:DocumentTypeCode>130</cbc:DocumentTypeCode> (3)

</cac:AdditionalDocumentReference>| 1 | Invoice object identifier scheme is given as an attribute on the identifier. It states the type of the identifier according to code list UN/CEFACT 1153 |

| 2 | An identifier of an object that the invoice relates to. |

| 3 | A code that qualifies the identifier as an invoiced object identifiers. Document type code "130" qualifies that. |

2.3.4. Contract reference

To reference or match an invoice to a purchase contract, the contract number could be specified like this:

<cac:ContractDocumentReference>

<cbc:ID>framework no 1</cbc:ID>

</cac:ContractDocumentReference>2.3.5. Despatch and receipt advice references

Document level

To reference or match an invoice to a despatch or receipt advice use the following elements:

<cac:DespatchDocumentReference>

<cbc:ID>despadv-3</cbc:ID> (1)

</cac:DespatchDocumentReference>

<cac:ReceiptDocumentReference>

<cbc:ID>resadv-1</cbc:ID> (2)

</cac:ReceiptDocumentReference>| 1 | Despatch advice |

| 2 | Receipt advice |

2.3.6. Tender reference

To identify the call for tender or lot the invoice relates to, use the 'OriginatorDocumentReference'. The identifier is, in most cases, the Procurement Procedure Identifier.

<cac:OriginatorDocumentReference>

<cbc:ID>ppid-123</cbc:ID>

</cac:OriginatorDocumentReference>2.3.7. Project reference

The project reference is optional to use, and is sent in an invoice in the element cac:ProjectReference/cbc:ID. In a credit note, this element does not exist, and project reference

is sent by using the element cac:AdditionalDocumentReference[cbc:DocumentTypeCode='50']/cbc:ID.

- NOTE

-

When sending the project reference, only the

cbc:IDand thecbc:DocumentTypeCodeare allowed in thecac:AdditionalDocumentReferenceelement.

<cac:ProjectReference>

<cbc:ID>project333</cbc:ID>

</cac:ProjectReference>2.3.8. Preceding invoice references

A credit note or negative invoice can refer to one or more initial invoice(s). This is done in the business group BG-3 Preceding invoice reference, providing the invoice number and issue date. The issue date shall be provided in case the preceding invoice reference is not unique.

In case correction applies to a large number of invoices, the invoicing period (BG-14), as necessary combined with a clarifying invoice note (IBT-22), may instead be given at document level.

2.3.9. Attachments

An invoice may contain a supportive document as informative. Examples of such documents may be work reports, certificates or other documents that relate to the purchase or the invoiced items. A supportive document can be attached to the invoice in two ways: by providing a direct hyperlink through which the document can be downloaded or by embedding the document into the invoice. A compliant receiver is required to be able to receive an attached supportive document and, in case of embedded files, to convert it into a file but he is not required to handle the content of that file since it is only provided as informative.

When attaching a document using an uri the hyperlink shall point directly to the file that is to be downloaded.

An embedded document is contained in the invoice as binary object using base64 encoding and shall be supplemented with information about the name of the document file and a mime code indicating the type of the file. This allows the receiver to convert the binary code into a file that has the same name as the original file and allows him to associate the received file to a suitable application for viewing its content. The set of allowed codes for the file type (mime code) is limited to types that can be opened with applications that are commonly used and available.

As is with other file types, when an attached file is an XML file the receiver is expected to be able to receive and convert the binary object into an XML file but the sender can not expect the receiver to view or process the content of that XML file. Any further handling of an embedded XML file attachment is optional for the receiver.

<cac:AdditionalDocumentReference>

<cbc:ID>ts12345</cbc:ID> (1)

<cbc:DocumentDescription>Technical specification</cbc:DocumentDescription> (2)

<cac:Attachment>

<cac:ExternalReference>

<cbc:URI>www.techspec.no</cbc:URI> (3)

</cac:ExternalReference>

</cac:Attachment>

</cac:AdditionalDocumentReference><cac:AdditionalDocumentReference>

<cbc:ID>mr4343</cbc:ID> (1)

<cbc:DocumentDescription>milage report</cbc:DocumentDescription> (2)

<cac:Attachment>

<cbc:EmbeddedDocumentBinaryObject mimeCode="text/csv" filename="milage.csv"

>bWlsYWdlIHJlcG9ydA==</cbc:EmbeddedDocumentBinaryObject> (4)

</cac:Attachment>

</cac:AdditionalDocumentReference>-

An identifier of the supporting document (ibt-122)

-

A description of the supporting document (ibt-123)

-

The URL (Uniform Resource Locator) that identifies where the external document is located (ibt-124)

-

An attached document embedded as binary object or sent together with the invoice. (ibt-125). The file type is given with the attribute "mimeCode" (ibt-125-1) and the name of the original file is given in the attribute "filename" (ibt-125-2).

2.3.10. Shipment, Delivery and Trade Terms

This section defines the representation and validation requirements for shipment-related information, customs references, import data, and Incoterms used in international trade transactions.

Overview

Shipment and trade-related data is represented using the following business terms.

| Business Term | Description | UBL Mapping |

|---|---|---|

BTOM-022 |

Incoterms |

|

BTOM-021 |

Customs Declaration Number |

|

BTOM-020 |

Import Date |

|

|

Shipment and delivery information is primarily relevant for import and export transactions. Validation requirements depend on the transaction type and applicable VAT treatment. |

Incoterms (BTOM-022)

Incoterms define the responsibilities of the buyer and seller in international trade, including delivery obligations, transfer of risk, and allocation of transportation costs.

Validation Rules

| Condition | Requirement |

|---|---|

Incoterms are provided |

|

Import transaction |

Incoterms MUST be provided as per business rule |

|

Only valid Incoterms codes defined by the International Chamber of Commerce (ICC), such as |

Shipment Information (BTOM-021)

Shipment data is represented using cac:Shipment.

Customs Declaration Number

The customs declaration number represents the customs authority reference associated with the import transaction.

Import Date (BTOM-020)

The import date represents the date on which goods were imported, delivered, or cleared through customs.

Transaction Type Dependencies

The requirement for shipment-related data is determined by the transaction type.

| Transaction Type | Requirement |

|---|---|

Import of Goods |

|

Export |

|

Other transactions |

|

|

Transaction type ( |

Validation Requirements

The following constraints MUST be satisfied.

| Validation Area | Requirement |

|---|---|

Shipment structure |

Shipment information MUST be represented under |

Customs declaration number |

Customs declaration number MUST use |

Import date |

Import date MUST use |

Incoterms structure |

|

Import transactions |

|

Data consistency |

Shipment-related data MUST be consistent with the transaction type and VAT treatment |

Legacy UUID Guidance

In specific business scenarios, references to previously issued invoices are mandatory, particularly for re-export and adjustment scenarios.

|

Where a referenced import invoice or prepayment invoice was issued prior to the implementation of mandatory e-invoicing and therefore does not contain a valid UUID, the following dummy UUID SHALL be used:

This dummy UUID SHALL only be used for references to legacy documents issued outside the e-invoicing system prior to go-live. If the referenced document contains a valid UUID, the actual UUID MUST be used. |

Compliance Principles

| Principle | Description |

|---|---|

Transaction-driven validation |

Shipment requirements depend on transaction type and VAT treatment |

Structural integrity |

Shipment information MUST follow the defined UBL hierarchy |

Trade standard compliance |

Incoterms MUST use internationally recognized codes |

Customs traceability |

Import transactions MUST contain sufficient customs references for audit and verification |

Data completeness |

Mandatory shipment information MUST be provided for import-related transactions |

Auditability |

Shipment, customs, and trade references MUST remain verifiable and traceable |

2.4. Allowances and Charges

The Invoice and credit note transactions has elements for Allowance/charge on 3 levels.

The element cac:AllowanceCharge with sub element cbc:ChargeIndicator indicates whether the instance is a charge (true) or an allowance (false).

- The header level

-

Applies to the whole invoice and is included in the calculation of the invoice total amount.

-

Several allowances and charges may be supplied

-

Specification of TAX for allowances and charges,

cac:TaxCategorywith sub elements, shall be supplied -

The sum of all allowances and charges on the header level shall be specified in

cbc:AllowanceTotalAmountandcbc:ChargeTotalAmountrespectively.

-

- The line level

-

Applies to the line level and is included in the calculation of the line amount.

-

Several allowances and charges may be supplied

-

Specification of TAX for allowances and charges shall not be specified, as the TAX category stated for the invoice line itself, applies also to the allowances or charges of that line.

-

The sum of all allowances and charges on the line level shall be taken into account, subtracted or added, when calculating the line extension amount . These line level allowances and charges shall not be calculated into the header level elements.

-

- The line level Price element

-

A way to inform the buyer how the price is set. Is also relevant if the seller or buyer want to post the allowance in their accounting systems. The price itself shall always be the net price, i.e. the base amount reduced with a discount (allowance).

-

Only one occurrence of allowance (discount) is allowed.

-

Specification of TAX for allowance shall not be specified

-

Allowance related to Price shall not be part of any other calculations.

-

Allowance related to Price may specify amount and the base amount.

-

<cac:AllowanceCharge>

<cbc:ChargeIndicator>true</cbc:ChargeIndicator> (1)

<cbc:AllowanceChargeReasonCode>FC</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Freight service</cbc:AllowanceChargeReason>

<cbc:MultiplierFactorNumeric>20</cbc:MultiplierFactorNumeric> (4)

<cbc:Amount currencyID="OMR">200</cbc:Amount> (5)

<cbc:BaseAmount currencyID="OMR">1000</cbc:BaseAmount> (3)

<cac:TaxCategory>

<cbc:ID>SR</cbc:ID>

<cbc:Percent>9</cbc:Percent>

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:TaxCategory>

</cac:AllowanceCharge>

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator> (2)

<cbc:AllowanceChargeReasonCode>65</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Production error discount</cbc:AllowanceChargeReason>

<cbc:Amount currencyID="OMR">300</cbc:Amount>

<cac:TaxCategory>

<cbc:ID>SR</cbc:ID>

<cbc:Percent>9</cbc:Percent>

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:TaxCategory>

</cac:AllowanceCharge>| 1 | ChargeIndicator = true to indicate a charge |

| 2 | ChargeIndicator = false to indicate an allowance |

| 3 | Base amount, to be used with the percentage to calculate the amount |

| 4 | Charge percentage |

| 5 | \$"Amount" = "Base amount" times ("Percentage" div 100)\$ |

<cac:InvoiceLine>

<!-- Code omitted for clarity -->

<cac:AllowanceCharge>

<cbc:ChargeIndicator>true</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>CG</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Cleaning</cbc:AllowanceChargeReason>

<cbc:MultiplierFactorNumeric>10</cbc:MultiplierFactorNumeric>

<cbc:Amount currencyID="OMR">1</cbc:Amount>

<cbc:BaseAmount currencyID="OMR">10</cbc:BaseAmount>

</cac:AllowanceCharge>

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>95</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Discount</cbc:AllowanceChargeReason>

<cbc:Amount currencyID="OMR">101</cbc:Amount>

</cac:AllowanceCharge>2.5. Payment means information

2.5.1. Credit transfer

| Payment means code 30 as defined below shall be supported by all receivers of a PINT compliant invoice. This payment method acts as the common denominator for global trade. |

If payment is made by credit transfer, the Payment account identifier (IBT-84) is mandatory

Examples of codes for payment by credit transfer are:

-

30 - Credit transfer

<cac:PaymentMeans>

<cbc:PaymentMeansCode name="Credit transfer">30</cbc:PaymentMeansCode>(1)

<cbc:PaymentID>93274234</cbc:PaymentID>(2)

<cac:PayeeFinancialAccount>

<cbc:ID>32423940</cbc:ID>(3)

<cbc:Name>AccountName</cbc:Name>

<cac:FinancialInstitutionBranch>

<cbc:ID>BIC32409</cbc:ID>(4)

</cac:FinancialInstitutionBranch>

</cac:PayeeFinancialAccount>

</cac:PaymentMeans>| 1 | Mandatory, payment means code for credit transfer |

| 2 | Remittance information |

| 3 | Mandatory, IBAN (in case of a SEPA payment) or a national account number (BBAN) |

| 4 | BIC or a national clearing code |

2.5.2. Card Payment

If the Buyer had opted to pay by using a payment card such as a credit or debit card, information on the Primary Account Number (PAN) shall be present in the invoice.

Examples of codes for payment by card are:

-

48 - Bank card

-

54 - Credit card

-

55 - Debit card

<cac:PaymentMeans>

<cbc:PaymentMeansCode name="Credit card">54</cbc:PaymentMeansCode>(1)

<cbc:PaymentID>9387439</cbc:PaymentID>

<cac:CardAccount>

<cbc:PrimaryAccountNumberID>123236</cbc:PrimaryAccountNumberID>(2)

<cbc:NetworkID>VISA</cbc:NetworkID>(3)

<cbc:HolderName>Card holders name</cbc:HolderName>(4)

</cac:CardAccount>

</cac:PaymentMeans>| 1 | Payment means code for credit card |

| 2 | Mandatory, shall be the last 4 to 6 digits of the payment card number |

| 3 | Mandatory, used to identify the financial service network provider of the card. Examples are VISA, MasterCard, American Express. |

| 4 | Card holder name |

2.6. Item information

2.6.1. Item identifiers

In an invoice line the seller item identifier, the buyer item identifier and the standard item identifier can be provided. For sellers and buyers item identifiers, no scheme attribute is used, whilst the schemeID

is mandatory for the standard item identification, and must be from the ISO 6523 ICD list.

<cac:BuyersItemIdentification>

<cbc:ID>b-13214</cbc:ID>

</cac:BuyersItemIdentification>

<cac:SellersItemIdentification>

<cbc:ID>97iugug876</cbc:ID>

</cac:SellersItemIdentification>

<cac:StandardItemIdentification>

<cbc:ID schemeID="0160">97iugug876</cbc:ID> (1)

</cac:StandardItemIdentification>| 1 | 0160 is the ICD value for a GTIN identifier |

2.6.2. Item classification

Several different item classification codes can be provided per invoice line, and the codes must be from one of the classification schemes in code list UNCL7143.

<cac:CommodityClassification>

<cbc:ItemClassificationCode listID="STI">09348023</cbc:ItemClassificationCode>(1)

</cac:CommodityClassification>| 1 | listID must be from UNCL7143 code list, and code STI indicates this is a CPV classification. |

<cac:CommodityClassification>

<cbc:ItemClassificationCode listID="TST" listVersionID="19.05.01">86776</cbc:ItemClassificationCode>(1)

</cac:CommodityClassification>| 1 | listID must be from UNCL7143 code list, and code TST indicates this is a UNSPSC classification, listVersionID is optional, but can be used to specify the version of UNSPSC. NOTE, in previous versions code MP was used as temporary workaround to identify UNSPSC. In fall release 2019 it is replaced with the new 7143 code TST that is specific for UNSPSC. |

2.7. Price information

An invoice must contain information about the item net price and additional information such as gross price, item price base quantity and price discount may be added.

For details on calculating price see Item net price (IBT-146).

<cac:Price>

<cbc:PriceAmount currencyID="OMR">410</cbc:PriceAmount> (4)

<cbc:BaseQuantity unitCode="C62">1</cbc:BaseQuantity> (3)

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator>

<cbc:Amount currencyID="OMR">40</cbc:Amount> (2)

<cbc:BaseAmount currencyID="OMR">450</cbc:BaseAmount> (1)

</cac:AllowanceCharge>

</cac:Price>| 1 | Item gross price |

| 2 | Item price discount |

| 3 | Item price base quantity |

| 4 | Item net price, must be equal to Item Gross price - item price discount (if these elements are used) |

<cac:Price>

<cbc:PriceAmount currencyID="OMR">200</cbc:PriceAmount>

<cbc:BaseQuantity unitCode="C62">2</cbc:BaseQuantity>

</cac:Price>2.8. Unit of measure

Unit of measure in an invoice allows the use of codes from UNECE Recommendation No. 20 (version 11e), as well as codes from UNECE Recommendation No. 21 prefixed with an X.

| Code | Name |

|---|---|

H87 |

Piece |

KGM |

Kilogram |

MTR |

Meter |

LTR |

Litre |

MTK |

Square metre |

MTQ |

Cubic metre |

KTM |

Kilometre |

TNE |

Tonne (metric ton) |

KWH |

Kilowatt hour |

DAY |

Day |

HUR |

Hour |

MIN |

Minute |

| Code | Name |

|---|---|

XBG |

Bag |

XBX |

Box |

XCT |

Carton |

XCY |

Cylinder |

XBA |

Barrel |

XPK |

Package |

XPX |

Pallet |

XRL |

Reel |

XSA |

Sack |

XST |

Sheet |

<cbc:InvoicedQuantity unitCode="C62">1</cbc:InvoicedQuantity> (1)

<cbc:InvoicedQuantity unitCode="XPX">1</cbc:InvoicedQuantity> (2)| 1 | Code H87 from Recommendation no. 20 |

| 2 | Code PX, prefixed with an X from Recommendation no. 21 |

3. Tax information

3.1. Tax in Accounting Currency

This section defines the representation and validation of VAT amounts when the invoice currency differs from the VAT accounting currency.

The purpose of these rules is to ensure accurate VAT reporting, currency consistency, and auditability in accordance with Oman VAT requirements.

3.1.1. General Principle

In Oman:

-

The VAT accounting currency MUST be

OMR -

Where the invoice currency differs from

OMR, VAT information MUST be represented in:-

Invoice currency

-

VAT accounting currency (

OMR)

-

|

The VAT accounting currency is used for tax reporting and reconciliation purposes. |

3.1.2. Currency Identification

The following business terms are used for currency handling.

| ID | Element | Description / Rule |

|---|---|---|

|

Invoice currency |

Currency used for invoice issuance and commercial amounts |

|

Tax accounting currency |

MUST be |

|

Exchange rate |

MUST be provided where invoice currency differs from tax accounting currency |

3.1.3. Currency Model

| Condition | Requirement |

|---|---|

Invoice currency = |

|

Invoice currency ≠ |

|

3.1.4. VAT Amount Representation

Two VAT amount representations are supported.

| Field | Description |

|---|---|

|

VAT amount in invoice currency |

|

VAT amount in VAT accounting currency ( |

3.1.5. Currency Conversion Rule

VAT amounts represented in VAT accounting currency MUST be derived using the exchange rate.

The following relationship applies:

VAT (OMR) ≈ Exchange Rate × VAT (Invoice Currency)|

The exchange rate:

|

3.1.6. Exchange Rate Constraints

The exchange rate MUST satisfy the following requirements.

| Validation Area | Requirement |

|---|---|

Source currency |

MUST match the invoice currency |

Target currency |

MUST match the VAT accounting currency ( |

Format |

|

3.1.7. VAT Consistency in Accounting Currency

Where VAT accounting currency is provided:

-

All VAT amounts in

cac:TaxTotalwithcurrencyID="OMR"MUST:-

Be consistently expressed in

OMR -

Match the aggregated VAT subtotals

-

Remain mathematically consistent with the exchange rate

-

3.1.8. VAT Breakdown Rules

3.1.9. VAT Category Rules

| Category | VAT Rate | Validation Rule |

|---|---|---|

|

|

VAT MUST be calculated and reported |

|

Exempt |

VAT amount MUST be |

|

Outside Scope |

VAT amount MUST be |

|

Zero Rated |

VAT amount MUST be |

|

VAT categories |

3.1.10. VAT Breakdown Grouping

Each VAT breakdown is uniquely identified by:

-

VAT category code

-

VAT rate

|

Differences in insignificant trailing decimals (for example |

3.1.11. Dual Currency VAT Example

The following UBL example demonstrates VAT represented in both invoice currency (EUR) and VAT accounting currency (OMR).

<cbc:DocumentCurrencyCode>EUR</cbc:DocumentCurrencyCode>

<cbc:TaxCurrencyCode>OMR</cbc:TaxCurrencyCode>

<cac:TaxTotal>

<cbc:TaxAmount currencyID="EUR">200.00</cbc:TaxAmount>

<cac:TaxSubtotal>

<cbc:TaxableAmount currencyID="EUR">4000.00</cbc:TaxableAmount>

<cbc:TaxAmount currencyID="EUR">200.00</cbc:TaxAmount>

<cac:TaxCategory>

<cbc:ID>S</cbc:ID>

<cbc:Percent>5</cbc:Percent>

</cac:TaxCategory>

</cac:TaxSubtotal>

</cac:TaxTotal>

<cac:TaxTotal>

<cbc:TaxAmount currencyID="OMR">167.58</cbc:TaxAmount>

</cac:TaxTotal>3.1.12. VAT Reporting Requirements

Invoices MUST provide sufficient VAT information to:

-

Enable accurate VAT reporting

-

Support audit verification

-

Ensure currency reconciliation

-

Support tax authority validation

Invoices MUST clearly identify:

-

VAT category

-

VAT calculation logic

-

Applied VAT treatment

-

VAT accounting currency where applicable

3.1.13. Compliance Principles

| Principle | Description |

|---|---|

Fixed VAT accounting currency |

VAT accounting currency is always |

Currency linkage |

Exchange rate governs consistency between invoice currency and VAT accounting currency |

Mathematical integrity |

VAT amounts MUST remain mathematically consistent across currencies |

Structural consistency |

VAT breakdown information MUST reconcile with invoice-level data |

Zero VAT enforcement |

VAT categories |

Auditability |

VAT calculations and currency conversions MUST remain traceable and verifiable |

3.1.14. Commodity classification (Specific to Oman)

PINT OM Billing supports the use of standardized commodity or service classification codes for identifying goods and services at invoice line level.

The classification code shall be provided using the UBL element cbc:ItemClassificationCode within cac:CommodityClassification.

The listID attribute shall contain a code from the UNCL7143 code list identifying the classification scheme used.

Supported classification schemes include:

-

HS — Harmonized System commodity codes

-

ISIC — International Standard Industrial Classification

-

UNGM service classification codes

-

Other classification schemes recognized by the Oman Tax Authority (OTA)

The structure and format of the classification code depend on the selected classification scheme.

Examples:

-

Oman HS commodity codes are represented using 12-digit codes

-

UNGM service classifications are represented using 8-digit codes

UBL example using HS classification

<cac:CommodityClassification>

<cbc:ItemClassificationCode listID="HS">847130000000</cbc:ItemClassificationCode>

</cac:CommodityClassification>UBL example using UNGM service classification

<cac:CommodityClassification>

<cbc:ItemClassificationCode listID="UNGM">72000000</cbc:ItemClassificationCode>

</cac:CommodityClassification>The value of the listID attribute determines the classification scheme applied to the item classification code.

The use of standardized classification schemes supports reporting, statistical, and analytical requirements defined by the Oman Tax Authority (OTA).

| The item classification code shall conform to the code structure and validation rules applicable to the selected classification scheme. |

4. Rules

The information given in a PINT invoice must comply to a set of rules on the content of the business terms as well as the relationship between them.

4.1. Calculations

4.1.1. Calculation of totals

Formulas for the calculations of totals are as follows:

| Business term id | Term name | Calculation |

|---|---|---|

IBT-106 |

Sum of invoice line net amounts |

\$sum("IBT-131: Invoice line net amount")\$ |

IBT-107 |

Sum of allowances on document level |

\$sum("IBT-92: Document level allowance amount")\$ |

IBT-108 |

Sum of charges on document level |

\$sum("IBT-99: Document level charge amount")\$ |

IBT-109 |

Invoice total amount without TAX |

\$\ \ \ \ "IBT-106: Sum of invoice line net amounts"\$ |

IBT-110 |

Invoice total TAX amount |

\$sum("IBT-117: TAX category tax amount")\$ |

IBT-112 |

Invoice total amount with TAX |

\$\ \ \ \ "IBT-109: Invoice total amount without TAX"\$ |

IBT-115 |

Amount due for payment |

\$\ \ \ \ "IBT-112: Invoice total amount with TAX"\$ |

4.1.2. UBL syntax calculation formulas

The following elements show the legal monetary totals for an invoice or credit note

| Element | Formula |

|---|---|

<cbc:LineExtensionAmount> |

\$sum("cac:InvoiceLine/cbc:LineExtensionAmount")\$ |

<cbc:AllowanceTotalAmount> |

\$sum("cac:AllowanceCharge[ChargeIndicator='false']/cbc:Amount")\$ |

<cbc:ChargeTotalAmount> |

\$sum("cac:AllowanceCharge[ChargeIndicator='true']/cbc:Amount")\$ |

<cbc:TaxExclusiveAmount> |

\$\ \ \ \ "cac:LegalMonetaryTotal/cbc:LineExtensionAmount"\$ |

<cbc:TaxInclusiveAmount> |

\$\ \ \ \ "cac:LegalMonetaryTotal/cbc:TaxExclusiveAmount"\$ |

<cbc:PrepaidAmount> |

Not applicable |

<cbc:PayableRoundingAmount> |

Not applicable |

<cbc:PayableAmount> |

\$\ \ \ \ "cac:LegalMonetaryTotal/cbc:TaxInclusiveAmount"\$ |

Element for rounding amount, the PayableRoundingAmount

It is possible to round the expected payable amount.

The element cac:LegalMonetaryTotal/cbc:PayableRoundingAmount is used for this purpose and is specified on the header level. This value shall be added to the value in cac:LegalMonetaryTotal/cbc:PayableAmount.

4.1.3. Calculation on line level

Item net price (IBT-146)

If gross price and discount exist, the Item net price has to equal with the item gross price less the item price discount.

Calculation formula:

\$"Item net price" = "Item gross price (IBT-148)" - "Item price discount (IBT-147)"\$

<cac:Price>

<cbc:PriceAmount currencyID="OMR">410</cbc:PriceAmount>(3)

<cbc:BaseQuantity unitCode="C62">1</cbc:BaseQuantity>

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator>

<cbc:Amount currencyID="OMR">40</cbc:Amount>(2)

<cbc:BaseAmount currencyID="OMR">450</cbc:BaseAmount>(1)

</cac:AllowanceCharge>

</cac:Price>| 1 | Item gross price |

| 2 | Item price discount |

| 3 | \$"Item price net amount" = "Item gross price" - "Item price discount"\$ |

Invoice line net amount (IBT-131)

The invoice line net amount (IBT-131) is as the name implies the net amount without TAX, and inclusive of line level allowance and charges.

The formula for calculating the invoice line net amount is:

\$"Item line net amount" = (("Item net price (IBT-146)" div "Item price base quantity (IBT-149)")\$

\$times ("Invoiced Quantity (IBT-129)")\$

\$+ "Invoice line charge amount (IBT-141)" - "Invoice line allowance amount (IBT-136)"\$

|

If the line net amount must be rounded to maximum decimals, please note that the different parts of the calculation must be rounded separately. I.e the result of: \$"Item line net amount" = (("Item net price (IBT-146)" div "Item price base quantity (IBT-149)") times ("Invoiced Quantity (IBT-129)")\$ must be rounded to maximum decimals, and the allowance/charge amounts are also rounded separately. |

<cbc:InvoicedQuantity unitCode="C62">10</cbc:InvoicedQuantity>(3)

<cbc:LineExtensionAmount currencyID="OMR">1000.00</cbc:LineExtensionAmount>(4)

<!-- Code omitted for clarity-->

<cac:Price>

<cbc:PriceAmount currencyID="OMR">200</cbc:PriceAmount>(1)

<cbc:BaseQuantity unitCode="C62">2</cbc:BaseQuantity>(2)

</cac:Price>| 1 | Item net price |

| 2 | Item price base quantity |

| 3 | Invoiced quantity |

| 4 | \$"Invoice line net amount" = (("Item net price" div "Item price base quantity") times ("Invoiced Quantity")\$ |

<cbc:InvoicedQuantity unitCode="C62">10</cbc:InvoicedQuantity>(4)

<cbc:LineExtensionAmount currencyID="OMR">900.00</cbc:LineExtensionAmount>(5)

<!-- Code omitted for clarity-->

<cac:AllowanceCharge>

<cbc:ChargeIndicator>true</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>CG</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Charge</cbc:AllowanceChargeReason>

<cbc:MultiplierFactorNumeric>1</cbc:MultiplierFactorNumeric>

<cbc:Amount currencyID="OMR">1</cbc:Amount>(2)

<cbc:BaseAmount currencyID="OMR">100</cbc:BaseAmount>

</cac:AllowanceCharge>

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>95</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Discount</cbc:AllowanceChargeReason>

<cbc:Amount currencyID="OMR">101</cbc:Amount>(3)

</cac:AllowanceCharge>

<!-- Code omitted for clarity-->

<cac:Price>

<cbc:PriceAmount currencyID="OMR">100</cbc:PriceAmount>(1)

</cac:Price>| 1 | Item net price |

| 2 | Line charge amounts |

| 3 | Line allowance amount |

| 4 | Invoiced quantity |

| 5 | \$"Invoice line net amount" = ("Item net price" times "Invoiced Quantity") + "line charge amount" - "line allowance amount"\$ |

4.1.4. Calculation of allowance/charge amount

Allowance and charge on document- and line level consists of elements carrying information on the allowance/charge base amount and the allowance/charge percentage. These are, if present in the invoice instance, used for calculating the allowance/charge amount.

If base amount is present, the percentage shall also be present, and if percentage is present, the base amount shall also be present, and the calculation of the amount shall be:

\$"Amount" = "Base amount" times ("Percentage" div 100)\$

<cac:AllowanceCharge>

<cbc:ChargeIndicator>true</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>CG</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Cleaning</cbc:AllowanceChargeReason>

<cbc:MultiplierFactorNumeric>20</cbc:MultiplierFactorNumeric>(2)

<cbc:Amount currencyID="OMR">200</cbc:Amount> (3)

<cbc:BaseAmount currencyID="OMR">1000</cbc:BaseAmount>(1)

<cac:TaxCategory>

<cbc:ID>SR</cbc:ID>

<cbc:Percent>9</cbc:Percent>

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:TaxCategory>

</cac:AllowanceCharge>| 1 | Base amount, to be used with the percentage to calculate the amount |

| 2 | Charge percentage |

| 3 | \$"Base amount" times ("Percentage" div 100) = "Amount"\$ |

<cac:AllowanceCharge>

<cbc:ChargeIndicator>false</cbc:ChargeIndicator>

<cbc:AllowanceChargeReasonCode>95</cbc:AllowanceChargeReasonCode>

<cbc:AllowanceChargeReason>Discount</cbc:AllowanceChargeReason>

<cbc:Amount currencyID="OMR">200</cbc:Amount>(1)

<cac:TaxCategory>

<cbc:ID>SR</cbc:ID>

<cbc:Percent>9</cbc:Percent>

<cac:TaxScheme>

<cbc:ID>VAT</cbc:ID>

</cac:TaxScheme>

</cac:TaxCategory>

</cac:AllowanceCharge>| 1 | Amount of allowance without calculations based on base amount and percentage |

4.2. Rounding

4.2.1. Shared rounding rules

A maximum of two digits are allowed for the following amounts in an invoice.

-

Document level allowance amount (ibt-092)

-

Document level charge amount (ibt-099)

-

Sum of allowances on document level (ibt-107)

-

Sum of charges on document level (ibt-108)

-

Invoice total amount without TAX (ibt-109)

-

Invoice total TAX amount (ibt-110)

-

Invoice total amount with TAX (ibt-112)

-

Amount due for payment (ibt-115)

4.3. Aligned calculations

This section explains how tax is calculated in the jurisdiction as well as other rules thar are specific to the jurisdiction.

4.3.1. Aligned Rounding

This section defines the rounding and rounding-tolerance behaviour applicable in PINT Oman for both Billing and Self-Billing.

Omani amounts are expressed in Omani Rial (OMR) using a three-decimal (Baisa) precision model, where 0.001 OMR = 1 Baisa. Document-level VAT amounts are expressed at two decimals, while line-level amounts are expressed at up to three decimals.

Baisa Gap Tolerance (Tax-Inclusive / B2C Scenarios)

In Omani retail environments, commercial prices are frequently expressed as tax-inclusive rounded values, whereas PINT calculations are derived using tax-exclusive arithmetic. Because of the three-decimal precision model, the backward derivation of a net amount from a tax-inclusive retail price can introduce a systematic rounding difference of one Baisa (0.001 OMR) per invoice line. This difference is referred to as the Baisa Gap.

PINT Oman absorbs this systematic difference through a bounded tolerance applied only to the VAT amount fields, without weakening the underlying validation. The tolerance is applied as follows.

| Field | Rule | Tolerance |

|---|---|---|

Line Item VAT amount ( |

|

|

VAT category tax amount ( |

|

|

|

The Baisa tolerance is confined to the VAT amount fields ( |

Validation Outcome Model

For the two VAT amount rules above, validation resolves to one of three outcomes. Each comparison is evaluated at the field’s native precision — three decimals for BTOM-016 (IBR-168-OM) and two decimals for IBT-117 (ALIGNED-IBRP-S-09-OM).

| Condition | Outcome | Validation behaviour |

|---|---|---|

The reported VAT amount equals the calculated amount exactly. |

Accepted |

No assertion is raised. |

The difference is non-zero but within tolerance. |

Accepted with warning |

The warning assertion ( |

The difference exceeds the tolerance. |

Rejected |

The fatal assertion ( |

|

Because the difference between two two-decimal amounts is a multiple of |

Rounding Amount (IBT-114) Handling

The Baisa tolerance is determined entirely from the invoice arithmetic and is applied independently of the Rounding Amount (IBT-114, PayableRoundingAmount). A sender is not required to report IBT-114 in order to benefit from the tolerance.

No restriction is placed on IBT-114: it is accepted as a free-form value and is not capped, equality-checked, or reconciled by any dedicated PINT Oman rule. This allows IBT-114 to absorb the systematic Baisa Gap together with other rounding-off differences (for example, those arising from exchange-rate conversion). Any residual difference MAY be recorded in IBT-114 for audit traceability, but doing so is optional.

|

The Tolerance-applied indicator business terms ( |

Worked Example (Baisa Gap)

| Component | Amount |

|---|---|

Retail price (tax-inclusive) |

|

Derived net price ( |

|

Line VAT amount ( |

|

Invoice line total ( |

|

Customer actually paid |

|

Difference (Baisa Gap) |

|

4.3.2. Aligned Calculations

This section defines the VAT calculation and validation principles applicable in PINT Oman.

The rules in this section ensure mathematical consistency, VAT integrity, and alignment between invoice content and VAT reporting structures.

VAT Category Behaviour

Each VAT category imposes specific calculation and reporting requirements.

| Category | Description | VAT Amount Rule |

|---|---|---|

|

Standard Rated |

VAT MUST be calculated using the applicable VAT rate of |

|

Exempt |

VAT amount MUST be |

|

Outside Scope |

VAT amount MUST be |

|

Zero Rated |

VAT amount MUST be |

|

VAT categories |

|

The category |

Mixed VAT Treatments

Invoices MAY contain multiple VAT treatments within the same document.

Typical combinations include:

-

Standard Rated (

S) -

Exempt (

E) -

Outside Scope (

O) -

Zero Rated (

Z)

Each VAT category MUST:

-

Be clearly identified at invoice line level

-

Be consistently represented in the VAT breakdown

-

Remain mathematically consistent with source amounts

VAT Breakdown Requirements

Category-Specific Rules

Exempt (E)

The following rules apply to VAT category E.

| Validation Area | Requirement |

|---|---|

VAT amount ( |

MUST be |

Taxable amount |

MUST equal: |

Simplified invoice |

VAT breakdown MAY be omitted |

Zero Rated (Z)

The following rules apply to VAT category Z.

| Validation Area | Requirement |

|---|---|

VAT amount ( |

MUST be |

Taxable amount |

MUST equal: |

Outside Scope (O)

The following rules apply to VAT category O.

| Validation Area | Requirement |

|---|---|

VAT amount |

MUST be |

Taxable amount |

MUST remain mathematically consistent with source values |

Simplified invoice |

VAT breakdown MAY be omitted |

Standard Rated (S)

The following rules apply to VAT category S.

| Validation Area | Requirement |

|---|---|

VAT rate |

MUST be exactly |

VAT breakdown grouping |

EXACTLY ONE VAT breakdown MUST exist for each distinct VAT rate |

|

Differences in insignificant trailing decimals (for example |

VAT Breakdown Example

The following UBL example demonstrates a VAT breakdown containing multiple VAT categories.

<cac:TaxTotal>

<cbc:TaxAmount currencyID="OMR">250.00</cbc:TaxAmount>

<cac:TaxSubtotal>

<cbc:TaxableAmount currencyID="OMR">5000.00</cbc:TaxableAmount>

<cbc:TaxAmount currencyID="OMR">250.00</cbc:TaxAmount>

<cac:TaxCategory>

<cbc:ID>S</cbc:ID>

<cbc:Percent>5</cbc:Percent>

</cac:TaxCategory>

</cac:TaxSubtotal>

<cac:TaxSubtotal>

<cbc:TaxableAmount currencyID="OMR">2000.00</cbc:TaxableAmount>

<cbc:TaxAmount currencyID="OMR">0</cbc:TaxAmount>

<cac:TaxCategory>

<cbc:ID>E</cbc:ID>

</cac:TaxCategory>

</cac:TaxSubtotal>

</cac:TaxTotal>Calculation Integrity Rules

The following calculation integrity principles apply.

| Validation Area | Requirement |

|---|---|

VAT consistency |

VAT amounts MUST reconcile with taxable amounts and VAT rates |

Breakdown integrity |

VAT breakdowns MUST reconcile with invoice lines, allowances, and charges |

Currency consistency |

VAT calculations MUST remain consistent across invoice and accounting currencies |

Duplicate grouping prevention |

Equivalent VAT rates MUST NOT create duplicate VAT breakdown groups |

Structural consistency |

VAT structures MUST follow the defined UBL hierarchy |

VAT Amount Rounding Tolerance (Baisa Gap)

For tax-inclusive (B2C) scenarios, a systematic one-Baisa (0.001 OMR) per-line rounding difference may arise when tax-exclusive values are derived backward from tax-inclusive retail prices. PINT Oman absorbs this difference through a bounded tolerance applied only to the VAT amount fields:

-

Line Item VAT amount (

BTOM-016,IBR-168-OM) —±0.001 OMRper invoice line, evaluated at three-decimal precision. -

VAT category tax amount (

IBT-117,ALIGNED-IBRP-S-09-OM) —±(0.001 × number of invoice lines) OMR, evaluated at two-decimal precision.

Each of these two rules produces a graduated outcome: an exact match is Accepted; a non-zero difference within tolerance is Accepted with warning (IBR-168-OM-WARN / ALIGNED-IBRP-S-09-OM-WARN), which does not reject the document; and a difference beyond tolerance is Rejected. Receivers MUST treat the warnings as informational.

The tolerance is applied independently of the Rounding Amount (IBT-114); IBT-114 is not required for the tolerance to apply and carries no cap, equality, or reconciliation constraint. The VAT category taxable amount (IBT-116, ALIGNED-IBRP-S-08-OM) and the invoice line total including VAT (BTOM-017, IBR-158-OM) do not carry the Baisa tolerance and retain standard two-decimal reconciliation.

|

Detailed rounding behaviour, the three-tier validation outcome model, and the |

Compliance Principles

| Principle | Description |

|---|---|

Data-driven VAT |

VAT MUST be derived from structured invoice data rather than manually entered values |

Structural consistency |

VAT breakdown information MUST accurately reflect invoice content |

Transaction-driven validation |

Transaction type determines whether VAT breakdown information is mandatory |

Zero VAT enforcement |

VAT categories |

Mathematical integrity |

All VAT calculations MUST remain internally consistent and auditable |

Auditability |

VAT calculations and source values MUST remain traceable and verifiable |

5. Technical details

Following section provide technical details.

5.1. BIS Identifiers